-1162026812.png)

-1162026812.png)

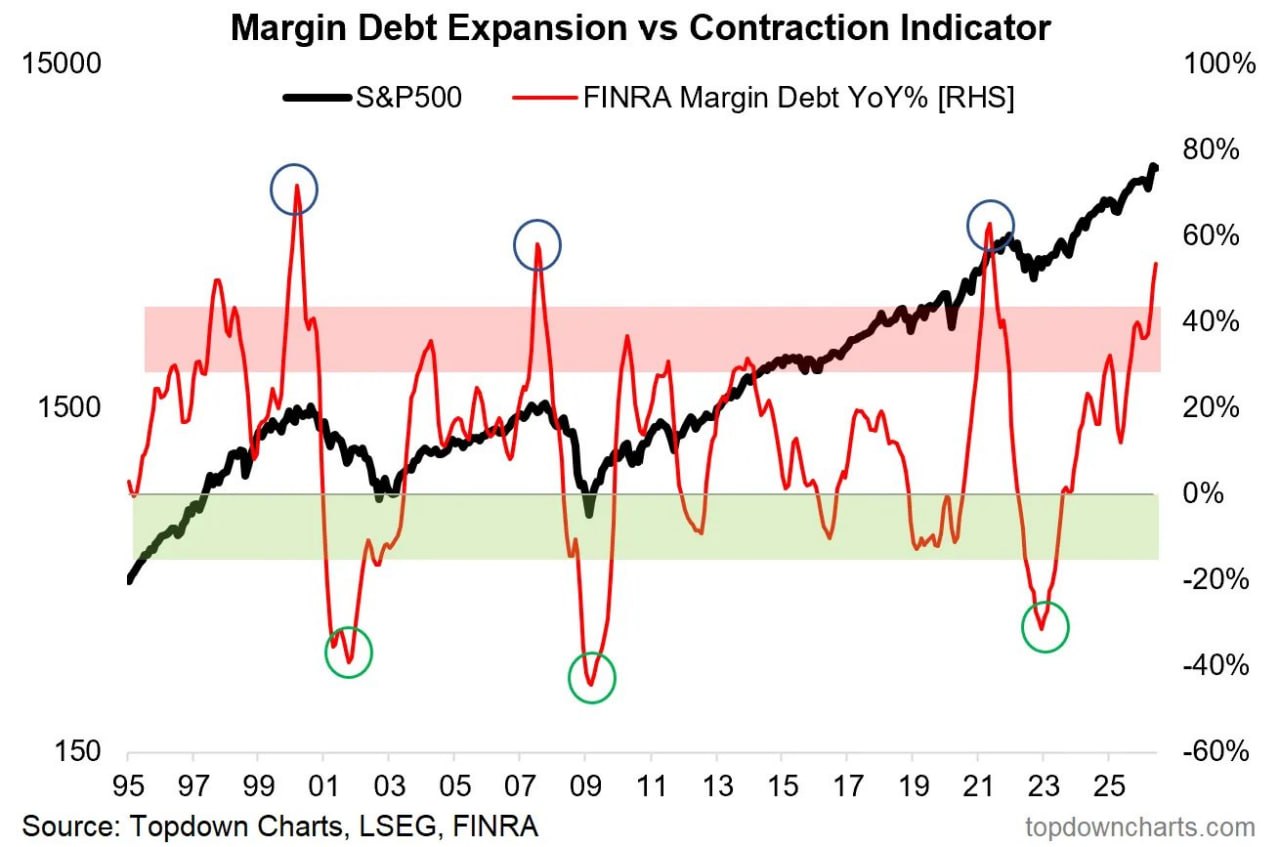

Margin Debt Is Flashing Red Again

This indicator had accurately signaled the three major market peaks of the past three decades and has just flashed another warning.

The growth in margin debt has reached levels that historically warrant attention. Margin debt refers to money borrowed by investors from brokers to purchase equities and other securities. Year-on-year growth accelerated from +53.3% in April to +53.7% in May.

Similar surges were observed ahead of the collapse of the "Nifty Fifty" era, the bursting of the dotcom bubble, the Global Financial Crisis of 2008 and the bear market of 2022.

Speculative activity continues to intensify, and historically such elevated levels of margin debt have not boded well for subsequent returns in the Nasdaq.

That said, high margin debt in itself does not cause markets to fall. Rather, it reflects investor sentiment and the growing willingness to assume risk. During powerful bull markets, leverage can fuel gains for far longer than sceptics expect, meaning these warning signals can remain present for months, if not quarters, before any meaningful reversal materializes.

It is also worth recognizing that the current cycle differs from previous episodes. Artificial intelligence, mega-cap technology companies and abundant liquidity remain the principal drivers of optimism. As long as the US economy remains resilient and corporate earnings continue to hold up, investor enthusiasm may persist considerably longer than history alone would suggest.

The conclusion is fairly straightforward. Elevated margin debt does not necessarily imply that a crash is imminent. What it does suggest is that markets are becoming increasingly vulnerable to disappointments and adverse surprises. The greater the amount of speculative capital supporting the rally, the more painful the eventual correction tends to be. At this stage, investors may wish to focus less on how much more they can make, and more on how much of their gains they can preserve should sentiment suddenly turn.

Today Technical Analysis: Gold falls below $4,100 and nears its yearly low as the USD pushes higher

Today Fundamental Analysis: Oil prices drop further as supply fears ease in response to the peace deal

Tech rout and Fed hike bets fuel global risk aversion

PMI Surges to Highest Since 2022; Dollar Index Climbs to One Year High

Post-FOMC Snapshot: Gold Navigates Dollar Strength and Rate Expectations

US100 – The AI Trade That Drove the Rally Is Starting to Crack

US Dollar Climbs to 13-Month Highs as Major Currencies Remain Under Pressure | 24th June, 2026