-21420261153.png)

-21420261153.png)

NFP Surprise Boosts the Dollar

Market Wrap-up: Strong US Payrolls Drive Dollar Higher and Pressure Risk AssetsMarket attention has shifted away from developments in the Middle East and toward the latest US labor market data. According to the US Bureau of Labor Statistics (BLS), Nonfarm Payrolls increased by 172,000 in May, more than double market expectations of approximately 85,000 jobs.

The unemployment rate remained unchanged at 4.3%, while the broader U6 unemployment measure declined to 8.1%. Meanwhile, annual average hourly earnings eased slightly to 3.4% from 3.6%.

April's payroll figure was also revised higher to 179,000, reinforcing the view that the US labor market remains resilient and shows little sign of deterioration.

Following the release, markets experienced broad based selling pressure across gold, oil, major currencies, and US equities as the US dollar surged to its highest level in nearly two months.

The US Dollar Index (DXY) broke above the key psychological 100.00 level, putting significant pressure on major currencies including the euro, British pound, and Japanese yen. Notably, USD/JPY moved above 160.00, a level where Japanese authorities have repeatedly warned they may intervene to counter excessive currency weakness.

Gold prices came under heavy selling pressure, falling nearly 2% to around $4,350/oz. US equity benchmarks including the Nasdaq, S&P 500, and Dow Jones also closed lower.

The stronger than expected payroll report prompted market participants to increase bets that the Federal Reserve may need to tighten policy further. On Kalshi's prediction market platform, the probability of a Fed rate hike this year surged from 25.3% to 52% within a week. Meanwhile, CME Group's FedWatch Tool currently reflects roughly a 50% chance of a rate increase before year end.

The data further supported gains in both the US dollar and Treasury yields. US government bond yields rose sharply across the curve on Friday, with the 2 year Treasury yield climbing more than 12 basis points while the benchmark 10-year yield advanced 6 basis points following the strong payrolls report.

In the energy market, WTI crude initially fell more than 2%. However, prices recovered nearly all of those losses after reports emerged that Iran had launched missiles toward Israel, clouding prospects for a broader peace agreement and reviving geopolitical risk premiums.

Looking ahead, this will be a critical week before major central banks enter their policy decision week. As a result, US inflation data including CPI and PPI will be closely scrutinized. Markets will also monitor Unemployment Claims, Preliminary University of Michigan Consumer Sentiment, and Inflation Expectations for further clues on the Fed's policy path.

XAU/USD: Gold Falls as Strong US Jobs Data Boosts Fed Rate Hike Expectations

Key takeaway:

Gold prices declined sharply on June 5 after US employment data significantly exceeded expectations, reinforcing the view that the Federal Reserve could keep interest rates elevated for longer amid persistent inflation concerns linked to Middle East tensions.

Higher interest rate expectations continue to increase the opportunity cost of holding non-yielding assets such as gold.

In addition, physical gold demand in India remained subdued this week, while gold premiums in China eased, providing limited support for prices.

Technical Outlook:

Daily Bias: Bearish

Support: 4,300 Resistance: 4,365

WTI: Oil Rebounds on Renewed Middle East Supply Risks

Key takeaway:

WTI crude prices advanced after Iranian missile attacks on Israel threatened a fragile ceasefire and raised concerns over energy supply disruptions in the Middle East.

Israeli airstrikes on Lebanon over the weekend further undermined peace prospects and delayed the normalization of critical oil flows through the Strait of Hormuz.

Meanwhile, OPEC+ approved a production quota increase of 188,000 barrels per day for July during Sunday's meeting.

Technical Outlook:

Daily Bias: Neutral

Support: 90.10Resistance: 95.70

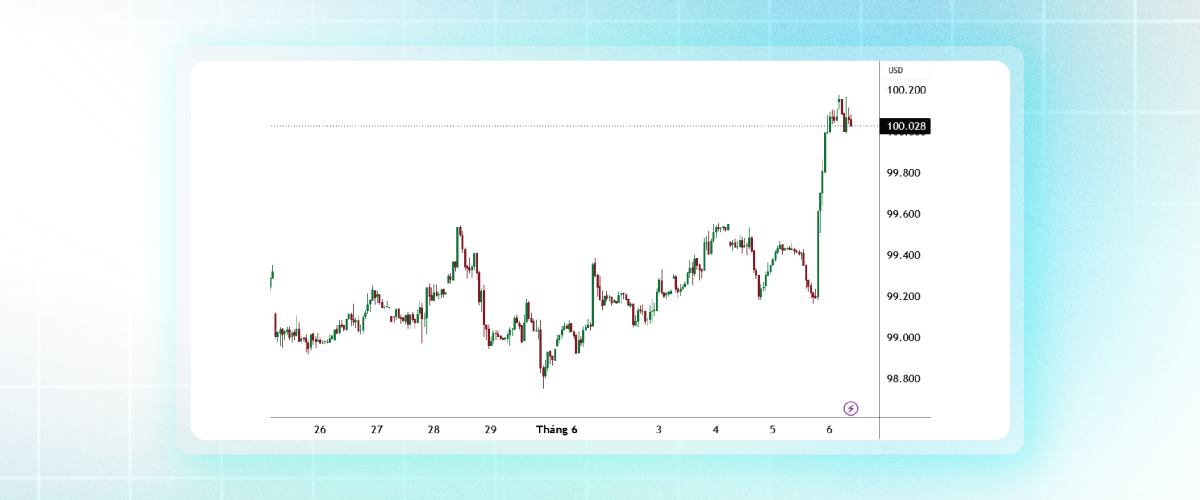

DXY: US Dollar Index Surges Following Strong Nonfarm Payrolls Report

Key takeaway:

The US Dollar Index surged after the Nonfarm Payrolls report delivered a decisive bullish surprise for the US dollar.

The payroll shock also came against the backdrop of increasingly hawkish Federal Reserve rhetoric.

Cleveland Fed President Hammack warned earlier last week that interest rates may need to rise rather than fall if inflation fails to moderate.

Technical Outlook:

Daily Bias: Bullish

Support: 99.54

Resistance: 99.70

EUR/USD: Euro Slides as Strong US Labor Data Strengthens the Dollar

Key takeaway:

The euro weakened sharply against a stronger US dollar following the payrolls report. However, downside pressure may be moderated by expectations that the European Central Bank will continue tightening policy, while geopolitical developments in the Middle East remain a source of uncertainty.

According to a Reuters survey of economists, the ECB is expected to raise its deposit rate to 2.25% at its June policy meeting, with another increase potentially following in September.

Technical Outlook:

Daily Bias: Bearish

Support: 1.15052

Resistance: 1.15761

USD/JPY: Japanese yen Breaks Above 160 as Dollar Rally Accelerates

Key takeaway:

The Japanese yen continued to weaken against the US dollar, with USD/JPY trading above the 160.00 threshold and keeping traders alert to potential intervention from Japanese authorities.

Japan's latest GDP data highlighted continued economic resilience, with the economy expanding 0.5% quarter-on-quarter.

The figure matched preliminary estimates, exceeded market expectations of 0.3%, and accelerated from the previous quarter's 0.2% growth, marking the strongest quarterly expansion since early 2025.

The stronger economic performance has reinforced expectations for further monetary policy normalization. Nevertheless, widening US-Japan yield differentials continue to favor the US dollar in the near term.

Technical Outlook:

Daily Bias: Bullish

Support: 160.20

Resistance: 160.00

The market narrative has shifted decisively from geopolitical headlines toward US macroeconomic strength. The stronger than expected NFP report triggered a broad repricing of Fed expectations, pushing Treasury yields and the US dollar sharply higher.

That repricing weighed on gold, pressured major currencies such as the euro and yen, and contributed to weakness across US equities. Oil remained the exception, as renewed tensions between Iran and Israel restored part of the geopolitical risk premium despite earlier losses.

For now, the dominant driver remains the outlook for US interest rates. Traders are increasingly focused on whether inflation data will validate the recent move higher in yields and reinforce expectations that the Fed could maintain a restrictive stance for longer.

The next major catalysts will be US CPI, PPI, Unemployment Claims, and the University of Michigan's Consumer Sentiment and Inflation Expectations reports. These releases are likely to shape market positioning ahead of next week's central bank meetings.

If you are looking for a platform to take advantage of market volatility, CPT Markets is a compelling choice. Trade global markets on advanced trading platforms with competitive spreads, fast execution, and a seamless experience across all devices.

Whether you are a beginner or an experienced trader, trading short-term or long-term, the right platform can make the difference - Trade smarter with CPT Markets!

This content is for informational purposes only and should not be considered investment advice. Trading financial products such as Forex and CFDs involves a high level of risk and may not be suitable for all investors. You may lose all of your invested capital. Please ensure that you fully understand the risks involved and carefully consider your financial situation before trading.

3.png "NFP Surprise Boosts the Dollar")

US Inflation in Focus as Euro Strengthens and Aussie Holds Near Two-Month Lows | 10th June, 2026

Faces Persistent Selling Pressure")

Gold (XAU/USD) Faces Persistent Selling Pressure

Middle East tensions spark market sell-off; all eyes on U.S. CPI tonight.

Dollar or Gold? Two Assets in Focus for the Second Half of 2026

Gold: has it bottomed out at $4,300?

Risk Sentiment Improves as Middle East Tensions Ease, CPI in Focus

XAUUSD Seeks Stability Ahead of Inflation Data